What the Straddle Options Strategy Really Offers

The straddle options strategy involves simultaneously buying a call option and a put option on the same underlying security, at the same strike price, with the same expiration date. This combination creates a position that profits when price moves significantly in either direction—you don't need to predict whether the stock will go up or down, only that it will move substantially. The strategy essentially transforms the question from "which way will it go?" to "will it move enough?" This shift in focus makes straddles uniquely suited for situations where you expect volatility but lack confidence in direction.

Why Traders Use Straddles

The straddle appeals to traders who recognize that sometimes the most honest assessment of a situation is uncertainty about direction combined with conviction about magnitude.

Before earnings announcements, FDA decisions, legal rulings, or major economic data releases, traders often sense that something significant will happen without knowing whether the outcome will be bullish or bearish. Traditional directional trades force you to guess—and being wrong means losing even if your volatility assessment was correct. The straddle removes this directional gamble. If you're right about the stock moving substantially, you profit regardless of which direction it moves. The winning side of your straddle gains more than the losing side costs, producing net profit. This structure allows you to act on volatility conviction without requiring directional conviction.

What This Article Covers

This article explains how the straddle options strategy works and how to use it effectively.

Topics this article will explain:

-

The structure of a straddle including strike selection and expiration considerations

-

The logic behind why straddles require significant movement to profit

-

The difference between long straddles and short straddles and their respective risk profiles

-

Ideal situations for deploying straddle strategies

-

How to calculate breakeven points and evaluate whether expected movement justifies the trade

-

How the Greeks affect your straddle position, particularly theta decay and vega exposure

-

The relationship between implied volatility and straddle pricing

-

Managing straddle positions including when to take profits and cut losses

-

Variations like strangles and how they compare to straddles

-

Common mistakes that undermine straddle profitability

The Bottom Line: The straddle options strategy allows you to profit from significant price movement without predicting direction, making it a powerful tool for situations where volatility is expected but the outcome remains genuinely uncertain—though this flexibility comes with costs and complexities that require understanding before deployment.

Understanding the Straddle Structure

The straddle options strategy has a straightforward construction: you buy one call option and one put option on the same underlying security, using the same strike price and the same expiration date. Both options are purchased simultaneously, creating a combined position that benefits from movement in either direction. The simplicity of the structure belies the sophistication of what it accomplishes—you're essentially buying volatility itself rather than betting on a particular price direction.

Strike Price and Expiration Selection

Most straddles use at-the-money strikes, meaning the strike price is at or very near the current price of the underlying stock.

At-the-money options have the highest time value and the most sensitivity to price movement in either direction, making them ideal for a strategy that profits from movement regardless of direction. If a stock trades at $100, a standard straddle would involve buying the $100 call and the $100 put with the same expiration. Both legs of the straddle expire on the same date, which is typically chosen to capture a specific expected event—like an earnings announcement—while minimizing unnecessary time decay. Shorter expirations cost less but leave less time for the move to develop, while longer expirations cost more but provide additional time for the thesis to play out.

Total Cost and Expiration Outcomes

The total cost of a straddle equals the premium paid for the call plus the premium paid for the put, and this combined cost determines your maximum loss and breakeven points.

How the straddle options position looks at expiration:

-

Your maximum loss equals the total premium paid for both options, occurring if the stock closes exactly at the strike price at expiration

-

If the stock moves above the strike, the call becomes valuable while the put expires worthless

-

If the stock moves below the strike, the put becomes valuable while the call expires worthless

-

You profit if the stock moves far enough in either direction to exceed the total premium paid

-

Upper breakeven equals the strike price plus total premium paid

-

Lower breakeven equals the strike price minus total premium paid

-

Between the two breakeven points, the position loses money at expiration, with maximum loss at the strike price

-

Beyond the breakeven points in either direction, profits are theoretically unlimited to the upside and substantial to the downside

-

One leg will always expire worthless or near worthless unless the stock closes exactly at the strike

The Logic Behind the Straddle

The straddle represents a fundamentally different kind of market opinion than most trades express. Instead of saying "I think this stock will go up" or "I think this stock will go down," the straddle says "I think this stock will move significantly, and I don't know which direction." This isn't a compromise or a hedge—it's a genuine expression of a specific market view. You're betting that volatility will exceed what the options market has priced in, regardless of whether that volatility manifests as a rally or a decline.

Betting on Movement, Not Direction

The straddle options strategy converts directional uncertainty into a tradeable position by focusing on magnitude rather than direction.

Why movement matters more than direction:

-

Both legs of the straddle start with value, and one will gain while the other loses as price moves

-

For the position to profit, the winning leg must gain more than the losing leg loses

-

This happens when price moves far enough that the winning option's gains exceed the total premium paid

-

Near the strike price, both options have roughly equal sensitivity to movement, so small moves produce minimal net change

-

As price moves substantially in one direction, the winning option accelerates in value while the losing option approaches zero

-

The losing option can only lose what you paid for it, while the winning option can gain much more

-

This asymmetry is what makes the strategy work—losses are capped but gains can expand significantly

The Relationship Between Cost and Required Move

The premium you pay for the straddle directly determines how much the stock must move for you to profit.

IF you buy a straddle for $10 total premium with a $100 strike price… THEN the stock must move above $110 or below $90 by expiration for you to profit.

IF implied volatility is high and the straddle costs $15 instead of $10… THEN breakeven points widen to $115 and $85, requiring a larger move to profit.

IF you buy a cheaper straddle with less time to expiration… THEN your cost is lower but you have less time for the expected move to occur.

IF the stock moves exactly to your upper breakeven of $110 at expiration… THEN your call is worth $10, your put is worthless, and you break even after paying $10 in premium.

IF the stock moves $20 above the strike to $120… THEN your call is worth $20, your put is worthless, and you profit $10 after subtracting the $10 premium.

IF the stock sits at $100 at expiration, exactly where it started… THEN both options expire worthless and you lose the entire $10 premium—your maximum loss.

When Uncertainty Becomes Opportunity

The straddle thrives in situations where genuine uncertainty about direction coincides with high probability of significant movement.

Earnings announcements represent the classic straddle opportunity because companies can surprise in either direction with meaningful stock reactions. The market knows the announcement is coming but cannot know whether results will exceed or miss expectations, or how the stock will react to guidance, commentary, or broader context. This uncertainty is reflected in elevated option premiums before earnings, but if actual movement exceeds what those premiums imply, straddle buyers profit. The same logic applies to FDA decisions, legal rulings, economic data releases, or technical setups where breakouts appear imminent but direction remains unclear. The straddle options strategy converts your honest acknowledgment of directional uncertainty into a position that profits from being right about volatility, even when you can't know which way the move will go.

Long Straddle vs. Short Straddle

The straddle options strategy comes in two forms that represent opposite bets on volatility. The long straddle involves buying both options and profits when price moves significantly. The short straddle involves selling both options and profits when price stays stable. These two approaches have completely different risk profiles, margin requirements, and suitable applications. Understanding both helps you see the full picture of what straddles offer, even if you only trade one side.

Long Straddle: Buying Movement

The long straddle is the strategy most traders think of when straddles are mentioned—buying a call and a put to profit from significant price movement in either direction.

Your maximum risk is limited to the total premium paid for both options. If the stock moves substantially, one option gains value while the other loses value, and if the move is large enough, your net position profits. Time works against you because both options lose value as expiration approaches if the stock hasn't moved. You need the stock to move beyond your breakeven points before expiration to profit, and the longer you hold without movement, the more theta decay erodes your position. The long straddle is a defined-risk position—you know exactly how much you can lose when you enter.

Short Straddle: Selling Stability

The short straddle involves selling both a call and a put at the same strike, collecting premium and hoping the stock stays near the strike price through expiration.

Risk profile of short straddles:

-

Maximum profit is limited to the premium collected, received upfront when you open the position

-

Maximum loss is theoretically unlimited to the upside and substantial to the downside

-

Time works in your favor as both options decay, increasing the probability that you keep the premium

-

You profit if the stock stays between the breakeven points through expiration

-

The position requires significant margin because of the undefined risk on both sides

-

Any significant move in either direction produces losses that can exceed the premium collected many times over

-

Short straddles are income strategies that work in low-volatility environments where movement is minimal

Why This Article Focuses on Long Straddles

The long straddle options strategy suits a broader range of traders because of its defined-risk profile and intuitive application before known volatility events.

Short straddles require margin approval, substantial account size, and active management to avoid catastrophic losses during unexpected moves. They're income strategies for experienced options traders comfortable with undefined risk. Long straddles, by contrast, have maximum loss capped at the premium paid, require no margin beyond the purchase price, and align naturally with identifiable events like earnings or data releases. For most traders looking to profit from expected volatility without directional conviction, the long straddle represents the appropriate application of this strategy.

When to Use a Straddle

The straddle options strategy works best in specific situations where uncertainty about direction coincides with high probability of significant movement. Not every volatile stock or uncertain situation justifies a straddle—the strategy requires that expected movement exceeds the cost of the position. Identifying the right situations for straddles means looking for catalysts that will force resolution one way or another, creating movement that exceeds what the options market has priced in.

Ideal situations for straddle options strategies:

-

Ahead of earnings announcements when a company's results could surprise significantly in either direction

-

Stocks with history of large earnings moves that exceed typical implied volatility pricing

-

Before major economic data releases like employment reports, inflation numbers, or Fed decisions that move entire sectors

-

Pending FDA decisions where approval or rejection will produce dramatically different stock reactions

-

Legal rulings or regulatory decisions with binary outcomes that could send the stock sharply higher or lower

-

Technical breakout setups where price has compressed into a tight range and a significant move appears imminent

-

Consolidation patterns like triangles, rectangles, or tight trading ranges that suggest energy building for a directional resolution

-

Merger or acquisition situations where deal completion or failure will produce substantial price movement

-

Product launches or major announcements where market reception remains genuinely uncertain

-

Any situation where you have strong conviction that the stock will move significantly but honest uncertainty about which direction

Matching the Strategy to the Situation

The common thread across all appropriate straddle situations is the combination of expected significant movement and genuine directional uncertainty.

If you have directional conviction, a straddle isn't the right tool—you're paying for exposure in a direction you don't believe in. If you don't expect significant movement, a straddle isn't the right tool—you need movement to overcome the cost of both options. The straddle options strategy occupies a specific niche: situations where something must happen, where that something will produce a substantial price reaction, and where predicting the direction of that reaction is genuinely difficult. Earnings announcements fit this profile perfectly for many stocks, which is why pre-earnings straddles represent the most common application. But any catalyst that forces resolution of uncertainty can create straddle opportunities if the expected movement justifies the premium paid.

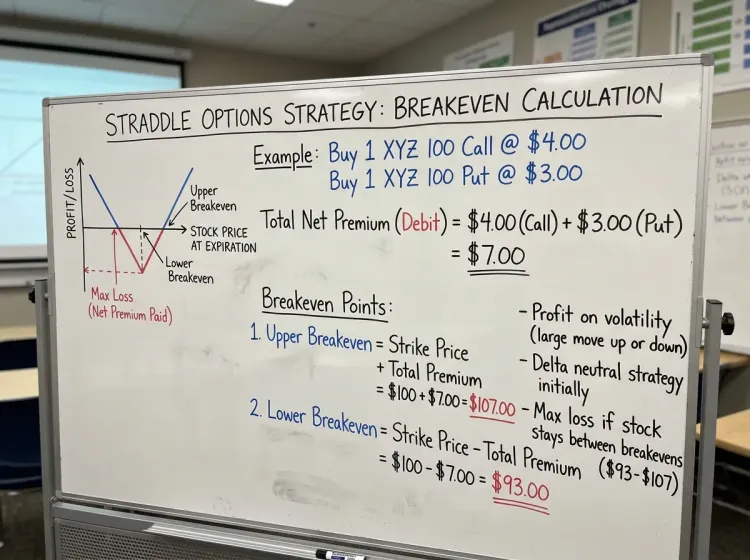

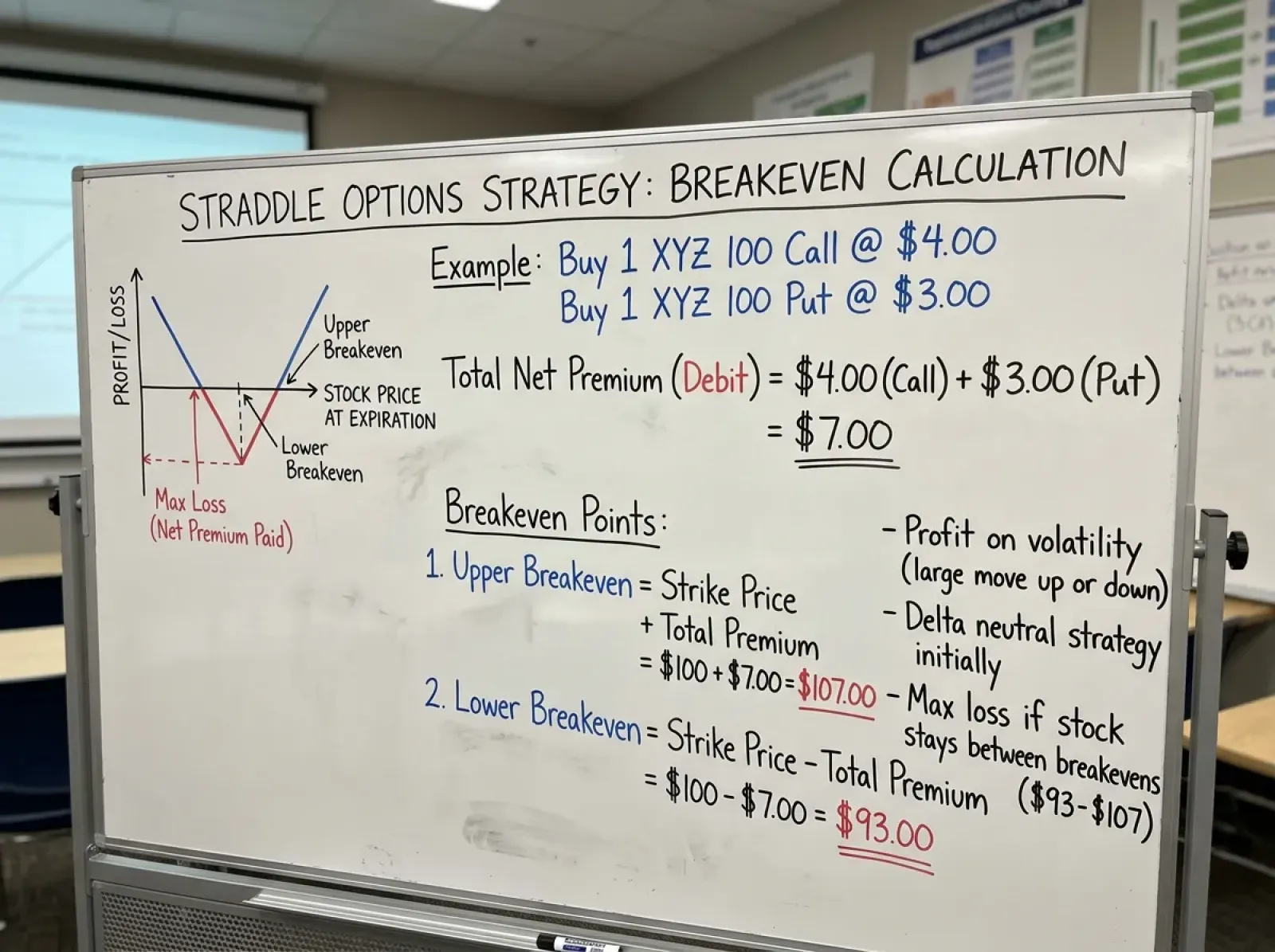

Calculating Breakeven Points

The breakeven points for a straddle options strategy define exactly how far the stock must move in either direction for you to avoid losing money at expiration. The upper breakeven equals the strike price plus the total premium paid for both options. The lower breakeven equals the strike price minus the total premium paid. If you buy a straddle with a $100 strike and pay $8 total ($4 for the call, $4 for the put), your upper breakeven is $108 and your lower breakeven is $92. The stock must close above $108 or below $92 at expiration for you to profit—any closing price between these two points results in a loss, with maximum loss occurring if the stock closes exactly at $100.

Why Breakeven Matters for Trade Selection

Understanding your breakeven points transforms the straddle from an abstract volatility bet into a concrete evaluation of whether the expected move justifies the cost.

Why breakeven calculation is fundamental to straddle trading:

-

Breakeven points tell you the minimum move required to profit, expressed in actual price terms

-

Converting breakeven to percentage terms allows comparison across different stock prices

-

A straddle on a $100 stock with $8 cost requires an 8% move to break even

-

A straddle on a $50 stock with $6 cost requires a 12% move to break even

-

Historical earnings moves and typical volatility can be compared directly to breakeven requirements

-

If a stock historically moves 5% on earnings and your breakeven requires 10% movement, the math doesn't favor the trade

-

Breakeven awareness prevents buying straddles that require unrealistic moves to profit

-

The distance between breakeven points represents the unprofitable zone you must escape

Evaluating Expected Movement

Before entering any straddle, compare your breakeven requirements to realistic expectations for how far the stock might actually move.

IF a stock typically moves 6% on earnings and your straddle breakeven requires 5% movement… THEN the expected move exceeds breakeven, suggesting favorable odds for the straddle.

IF a stock typically moves 4% on earnings and your straddle breakeven requires 7% movement… THEN the expected move falls short of breakeven, suggesting the straddle is overpriced for the likely outcome.

IF implied volatility has spiked significantly before the event, increasing straddle cost… THEN breakeven points widen, requiring a larger-than-typical move to profit even if volatility expectations are reasonable.

IF you can find historical data showing the stock has exceeded your breakeven distance on 60% of similar events… THEN the straddle options strategy offers positive expected value based on historical precedent.

IF the straddle costs 10% of the stock price but the largest move in the past eight quarters was 8%... THEN the options market is pricing in more movement than history supports, making the straddle expensive.

IF you cannot determine reasonable movement expectations from historical data or analysis… THEN you lack the information needed to evaluate whether the straddle offers value, and you're gambling rather than trading.

The Greeks and Your Straddle

The Greeks measure how different factors affect your option position's value, and understanding them helps you anticipate how your straddle will behave as conditions change. A straddle options strategy has a unique Greek profile because combining a call and put at the same strike creates characteristics that differ from either option alone. Some Greeks work in your favor while others work against you, and knowing which is which helps you manage the position effectively.

How each Greek affects your straddle:

-

Delta measures directional exposure, and an at-the-money straddle starts with near-zero delta because the call's positive delta roughly offsets the put's negative delta

-

As price moves up, the call gains delta while the put loses it, making your overall position increasingly bullish

-

As price moves down, the put gains negative delta while the call loses positive delta, making your position increasingly bearish

-

This shifting delta is actually what you want—the position becomes directional in whichever way the stock moves

-

Gamma measures how quickly delta changes with price movement, and straddles have high gamma at the money

-

High gamma means your position rapidly gains directional exposure as the stock moves, accelerating your profits if the move continues

-

Gamma is highest near expiration and near the strike price, which is when small moves create large delta changes

-

Theta measures time decay, and long straddles have negative theta—time works against you

-

Both options lose value each day as expiration approaches if the stock hasn't moved

-

Theta decay accelerates as expiration nears, making timing critical for straddle entries

-

Vega measures sensitivity to implied volatility changes, and long straddles have positive vega

-

If implied volatility rises after you buy the straddle, your position gains value even without price movement

-

If implied volatility falls—as it often does after events like earnings—your position loses value from the IV crush

Putting the Greeks Together

The Greek profile of a straddle options position reveals why timing, movement, and volatility all matter for profitability.

Your straddle starts delta-neutral but gains directional exposure through gamma as the stock moves. This is exactly what you want—the position aligns with whatever direction emerges. However, theta constantly erodes your position while you wait for movement, and vega exposure means that volatility contraction after an event can hurt you even if the stock moves in your favor. The ideal scenario combines quick, significant price movement with stable or rising implied volatility. The worst scenario combines no movement, extended holding period, and collapsing implied volatility.

Remember: The Greeks reveal that your straddle options strategy benefits from rapid price movement in either direction through high gamma, suffers from time passing without movement through negative theta, and remains vulnerable to implied volatility contraction through positive vega—making quick resolution of your volatility thesis the key to profitability.

Implied Volatility and Straddle Pricing

Implied volatility is the single most important factor determining what you pay for a straddle. IV represents the market's expectation for how much the underlying stock will move, and this expectation gets priced directly into option premiums. When the market expects big movement, IV rises and options become expensive. When the market expects stability, IV falls and options become cheap. Since a straddle involves buying two options, you're doubly exposed to IV levels—high IV means paying more for both the call and the put, widening your breakeven points and requiring larger moves to profit.

Why Straddles Are Expensive Before Events

The options market knows about scheduled events like earnings announcements, and this knowledge gets reflected in elevated implied volatility.

How IV affects straddle options pricing:

-

Before earnings, IV typically rises as traders anticipate the upcoming move

-

This elevated IV makes straddles more expensive precisely when traders most want to buy them

-

The market is essentially pricing in the expected earnings move, making it harder to profit from that move

-

If a stock typically moves 5% on earnings, IV will rise to reflect approximately that expected movement

-

To profit from an earnings straddle, the actual move must exceed what IV has already priced in

-

IV expansion before events protects option sellers and creates a hurdle for straddle buyers

-

Stocks with histories of large earnings surprises tend to have higher pre-earnings IV than stable earners

-

The IV premium before events represents the market's collective estimate of coming volatility

IV Crush After Announcements

After the anticipated event occurs, implied volatility typically collapses rapidly as uncertainty resolves—a phenomenon called IV crush that can devastate straddle positions.

DO understand that IV crush happens immediately after events, often overnight, and cannot be avoided by quick selling.

DO calculate how much IV crush will affect your position by comparing pre-event IV to typical post-event IV levels.

DO recognize that the stock must move enough to overcome both the breakeven distance and the IV crush impact.

DO consider buying straddles before IV has fully expanded if you anticipate an event the market hasn't fully priced.

DO look for situations where you expect movement to exceed what elevated IV implies.

DON'T assume that a big stock move guarantees straddle profit—IV crush can offset significant price movement.

DON'T buy straddles at peak IV right before announcements without accounting for the post-event volatility collapse.

DON'T ignore the difference between current IV and historical IV when evaluating straddle options pricing.

DON'T expect to exit straddles after events at pre-event IV levels—the crush is immediate and unavoidable.

DON'T buy straddles simply because an event is approaching without comparing the cost to realistic movement expectations.

Managing a Long Straddle Position

Opening a straddle options position is only half the challenge—managing it effectively determines whether your volatility thesis translates into actual profits. Unlike directional trades where the exit decision is relatively straightforward, straddles present unique management questions. You have two legs moving in opposite directions, time decay constantly eroding value, and the possibility of continued movement that might justify holding longer. Having a management plan before you enter prevents emotional decision-making when real money is on the line.

Management considerations for straddle positions:

-

Decide before entry what profit level would trigger taking gains on the winning leg

-

Determine whether you'll close the entire position at once or leg out by selling one side first

-

Set a maximum loss threshold as a percentage of premium paid, not just "when it expires worthless"

-

Consider time-based exits if the expected catalyst hasn't produced movement within a reasonable window

-

Plan for different scenarios: quick move, gradual move, no move, move then reversal

-

Understand that holding through time decay without movement is a choice with costs

-

Recognize when the thesis has played out versus when additional upside remains possible

When to Take Profits on the Winning Leg

The decision to close the profitable side of your straddle involves balancing captured gains against potential additional movement.

Questions to ask yourself when managing a winning straddle:

-

Has the catalyst I anticipated already occurred, or is there potential for additional volatility?

-

How much of my maximum potential profit have I captured, and am I being greedy by holding for more?

-

Is implied volatility still elevated or has IV crush already occurred, limiting further option gains?

-

How much time remains until expiration, and is theta decay now significant for my remaining position?

-

If I close the winning leg and hold the losing leg, am I creating a directional bet I actually want?

Handling the Losing Leg

The losing leg of your straddle will decay toward zero if the stock continues in the direction that favors your winner, but it retains value if there's time remaining and a reversal remains possible.

Many traders close the entire straddle at once rather than legging out, which avoids the complexity of managing a single remaining option. If you sell only the winning leg, you're left with an out-of-the-money option that needs a reversal to become valuable—essentially a new directional bet. This can make sense if the initial move seems exhausted and reversal seems likely, but it requires a new thesis rather than just continuation of your original volatility view. Some traders sell the losing leg first when a small bounce occurs, then hold the winning leg for potential continuation, but this requires precise timing and active management.

Rolling and Loss Thresholds

Rolling involves closing your current straddle and opening a new one at different strikes or expirations to capture additional movement or repair a losing position.

Pro tip: If the stock has moved significantly toward one of your breakeven points but the catalyst hasn't fully played out, rolling to a new at-the-money straddle can reset your position to capture additional movement in either direction.

Pro tip: Set a maximum loss threshold—such as 50% of premium paid—at which you exit the straddle options position regardless of time remaining, preventing the full loss that occurs if you hold to worthless expiration without movement.

Remember: Managing a straddle options position requires advance planning for profit-taking, loss limits, and whether to exit the entire position or leg out—and having these decisions made before entry prevents emotional management that typically leads to holding losers too long and cutting winners too short.

Straddle Variations

The classic straddle options strategy uses at-the-money strikes for both the call and put, but variations exist that modify the structure to match different outlooks, budgets, and risk tolerances. Understanding these variations helps you select the right tool for each situation rather than forcing the standard straddle into every volatility trade. The most common variation is the strangle, which uses different strikes to reduce cost while accepting wider breakeven points.

Straddle variations and modifications:

-

The strangle uses out-of-the-money strikes—a call above current price and a put below—reducing total premium paid

-

Lower cost means lower maximum loss but also wider breakeven points requiring larger moves to profit

-

Straddles can be constructed with slightly in-the-money options for increased delta sensitivity at higher cost

-

Strike selection can be skewed if you have directional lean while still wanting exposure to movement in both directions

-

Weekly expirations offer lower premium but less time for the move to develop and faster theta decay

-

Monthly or longer expirations cost more but provide additional time and slower daily decay

-

Ratio straddles involve unequal quantities of calls and puts, creating directional bias within the volatility structure

-

Calendar straddles sell near-term options while buying longer-term options at the same strike

Comparing Straddles and Strangles

The choice between a straddle and a strangle depends on your cost tolerance, movement expectations, and how far you believe the stock might move.

A straddle costs more because at-the-money options have higher premiums, but its breakeven points are narrower, requiring a smaller move to profit. A strangle costs less because out-of-the-money options are cheaper, but both legs need the stock to move significantly before either gains intrinsic value. If you expect a massive move—well beyond what the straddle would require—the strangle offers better return on capital because you pay less for similar upside. If you expect a moderate move that barely exceeds breakeven, the straddle gives you a better chance of capturing it because your breakevens are closer to current price.

Expiration Selection

The expiration you choose for your straddle options strategy affects cost, time decay rate, and how much time you have for your volatility thesis to play out.

Weekly options cost less and experience rapid theta decay, making them appropriate when you expect an immediate catalyst with quick resolution. Monthly options cost more but decay more slowly early in their life, giving you additional time if the expected move takes longer to develop. For earnings plays, traders typically use the expiration closest to the announcement date that still captures the event—this minimizes time value paid for days after the catalyst has passed. For technical breakout setups where timing is less certain, longer expirations provide cushion against being early on your volatility call.

Quick tip: When trading earnings straddles, use the weekly expiration that captures the announcement rather than paying extra for monthly options that include many post-earnings days you don't need.

Quick tip: Consider strangles over straddles when implied volatility is particularly elevated, as the lower cost of out-of-the-money options partially offsets the inflated premium environment.

Keep In Mind: The straddle options strategy is just one variation in a family of volatility structures, and matching the specific variation—standard straddle, strangle, skewed strikes, weekly or monthly expiration—to your outlook and cost tolerance produces better results than applying the same structure to every situation.

Common Straddle Trading Mistakes

The straddle options strategy appears straightforward—buy a call and a put, wait for movement, profit from volatility. But this simplicity masks complexities that cause traders to lose money consistently. The most common mistakes involve paying too much for straddles, underestimating what's required to profit, or holding positions through conditions that guarantee losses. Recognizing these errors before you make them saves both capital and frustration.

Common mistakes when trading straddles:

-

Buying straddles when implied volatility is already elevated, paying premium prices for options that will experience IV crush after the event

-

Failing to compare current IV to historical IV levels to determine whether straddles are expensive or reasonably priced

-

Assuming that high IV means big moves are coming rather than recognizing that high IV means big moves are already priced in

-

Underestimating the move required to profit by not calculating breakeven points before entering

-

Being surprised that a 5% move didn't produce profits when breakeven required 8% movement

-

Ignoring that both legs cost money and the stock must move beyond the combined premium to generate returns

-

Holding through time decay without movement, watching theta erode position value while hoping for a move that isn't coming

-

Failing to set time-based exits that acknowledge when the thesis has failed rather than waiting for worthless expiration

-

Treating the maximum loss as acceptable without considering that partial loss exits preserve capital for better opportunities

-

Ignoring the cost of the trade relative to expected movement, buying straddles that require historically unprecedented moves

-

Not researching how much the underlying typically moves on similar events before committing capital

-

Assuming that expensive straddles indicate smart money expecting huge moves rather than recognizing that demand has inflated pricing

-

Trading straddles on low-volatility underlyings that rarely move enough to exceed breakeven points

-

Applying the straddle options strategy to stable stocks, ETFs, or indices without considering their typical movement ranges

-

Expecting index straddles to behave like individual stock straddles despite indices having naturally dampened volatility

-

Buying straddles without a specific catalyst, just hoping that something will happen to create movement

-

Holding through the catalyst when the move doesn't materialize, adding time decay to the already-failed thesis

-

Refusing to take partial losses because it feels like admitting defeat, resulting in larger losses at expiration

-

Overtrading straddles around every minor event rather than selecting situations where the strategy has genuine edge

Making the Straddle Options Strategy Work for You

The straddle options strategy occupies a unique place in your trading toolkit—it's the answer to the specific question of what to do when you expect significant movement but genuinely cannot determine direction. This isn't a default strategy or a way to avoid making directional decisions. It's a precision tool for situations where volatility conviction exceeds directional conviction, where catalysts demand resolution, and where the cost of the position is justified by realistic movement expectations. Used appropriately, straddles allow you to profit from being right about volatility without the penalty of being wrong about direction.

Building Straddles Into Your Toolkit

The straddle options strategy becomes valuable when you treat it as one tool among many rather than a universal solution or a way to hedge your uncertainty on every trade.

Most trading situations don't call for straddles. When you have directional conviction, directional trades offer better risk-reward. When you don't expect significant movement, straddles guarantee losses through time decay. The strategy fits a specific niche: genuine directional uncertainty combined with high conviction about magnitude, typically ahead of known catalysts with binary outcomes. Building straddles into your toolkit means identifying these situations consistently, evaluating whether the cost is justified by realistic movement expectations, and managing positions with predetermined rules rather than emotional reactions.

Maintain realistic expectations—straddles won't win every time, IV crush erodes gains even on correct volatility calls, and the options market is generally efficient at pricing expected moves. Your edge comes from identifying situations where actual movement will exceed priced-in expectations, entering at reasonable IV levels, and managing positions to capture gains while limiting losses when the thesis doesn't play out.