What the Covered Call Strategy Can Do for Your Portfolio

The covered call strategy offers something that appeals to almost every stock investor: the ability to generate income from shares you already own. Instead of waiting passively for dividends or price appreciation, you can actively collect premium by selling call options against your existing holdings. This transforms a buy-and-hold position into an income-producing asset, putting cash in your account regardless of whether the stock moves up, down, or sideways. For investors frustrated by stagnant positions or seeking to enhance returns in range-bound markets, covered calls provide a structured way to extract value from shares that might otherwise just sit there.

The Trade-Off You're Making

Every financial strategy involves trade-offs, and covered calls are no exception—the income you receive comes at the cost of capping your upside potential.

When you sell a call option against your shares, you're giving someone else the right to buy those shares from you at a specific price (the strike price) before a specific date (expiration). In exchange, you receive premium immediately. If the stock stays below the strike price, you keep both your shares and the premium. If the stock rises above the strike price, your shares may be called away, meaning you sell them at the strike price regardless of how much higher the market price has climbed. You still profit—you keep the premium plus any gains up to the strike—but you miss out on appreciation beyond that level. This trade-off defines the covered call strategy: you're exchanging unlimited upside potential for immediate, tangible income.

What This Article Covers

This article explains how to implement covered calls effectively, from understanding the basic mechanics to managing positions and avoiding common mistakes.

Topics this article will cover:

-

The mechanics of covered calls and why the strategy is considered conservative relative to other options approaches

-

How to structure a covered call trade including stock selection, strike price, and expiration date

-

Strike price selection strategies for different market outlooks and income goals

-

How expiration timing affects premium received and assignment probability

-

Calculating potential returns, maximum profit, and breakeven points

-

Market conditions where covered calls perform best and where they struggle

-

Position management techniques including rolling, early buyback, and handling assignment

-

Common mistakes that erode covered call returns and how to avoid them

Understanding the Covered Call

A covered call is an options strategy that combines two positions: owning shares of a stock and selling call options against those shares. The strategy generates immediate income in the form of option premium while obligating you to potentially sell your shares at a predetermined price. Unlike speculative options strategies that involve complex multi-leg positions or naked exposure, the covered call strategy ranks among the most conservative options approaches because your obligation to deliver shares is backed by actual ownership of those shares.

The basic mechanics of a covered call:

-

You own at least 100 shares of a stock (options contracts represent 100 shares each)

-

You sell one call option contract for every 100 shares you own

-

You receive premium immediately when you sell the call

-

The call gives the buyer the right to purchase your shares at the strike price before expiration

-

If the stock stays below the strike price at expiration, the option expires worthless and you keep both shares and premium

-

If the stock rises above the strike price, your shares may be assigned (sold) at the strike price

-

Your profit in the assignment scenario equals the strike price minus your cost basis, plus the premium received

Why It's Called Covered

The term "covered" distinguishes this strategy from its far riskier cousin, the naked call, and explains why brokers allow it in retirement accounts and conservative portfolios.

When you sell a call option without owning the underlying shares, you've sold a "naked" call—you're exposed to theoretically unlimited losses because you'd have to buy shares at whatever market price to deliver them if assigned. If a stock doubles or triples, your losses could be catastrophic. A covered call eliminates this risk entirely because you already own the shares you might need to deliver. Your maximum loss comes from the stock declining, not from the short call position, and that stock ownership risk exists whether you sell calls against it or not. The covered position means your obligation is fully backed by existing assets, making this one of the few short option strategies considered appropriate for conservative investors.

How Premium Collection Works

When you sell a call option, the buyer pays you premium upfront, and this cash hits your account immediately regardless of what happens afterward.

Option premium represents the price the buyer pays for the right to purchase shares at the strike price. This premium belongs to you the moment the trade executes.

IF the stock price stays below the strike price through expiration… THEN the call expires worthless, you keep your shares, you keep the full premium, and you can sell another call to collect more premium.

IF the stock price rises above the strike price at expiration… THEN the call will likely be exercised, you sell your shares at the strike price, you keep the full premium, and your position ends.

IF the stock price drops significantly… THEN the call expires worthless, you keep the premium which partially offsets your unrealized loss, and you still own shares that have declined in value.

IF you want to exit the position before expiration… THEN you can buy back the call option at its current market price, closing the obligation and freeing your shares.

IF the stock rises above the strike price but you don't want to sell your shares… THEN you can buy back the call at a loss and either keep your shares or roll to a new position at a higher strike or later expiration.

The Bottom Line: The covered call strategy combines stock ownership with call option selling to generate immediate premium income, with the "covered" designation meaning your short option obligation is backed by shares you already own—making this a conservative approach to options that's accessible even to investors who typically avoid derivative strategies.

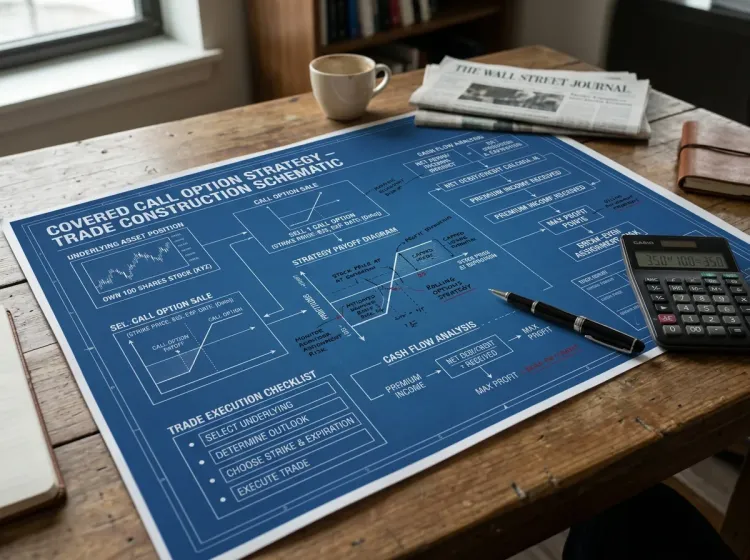

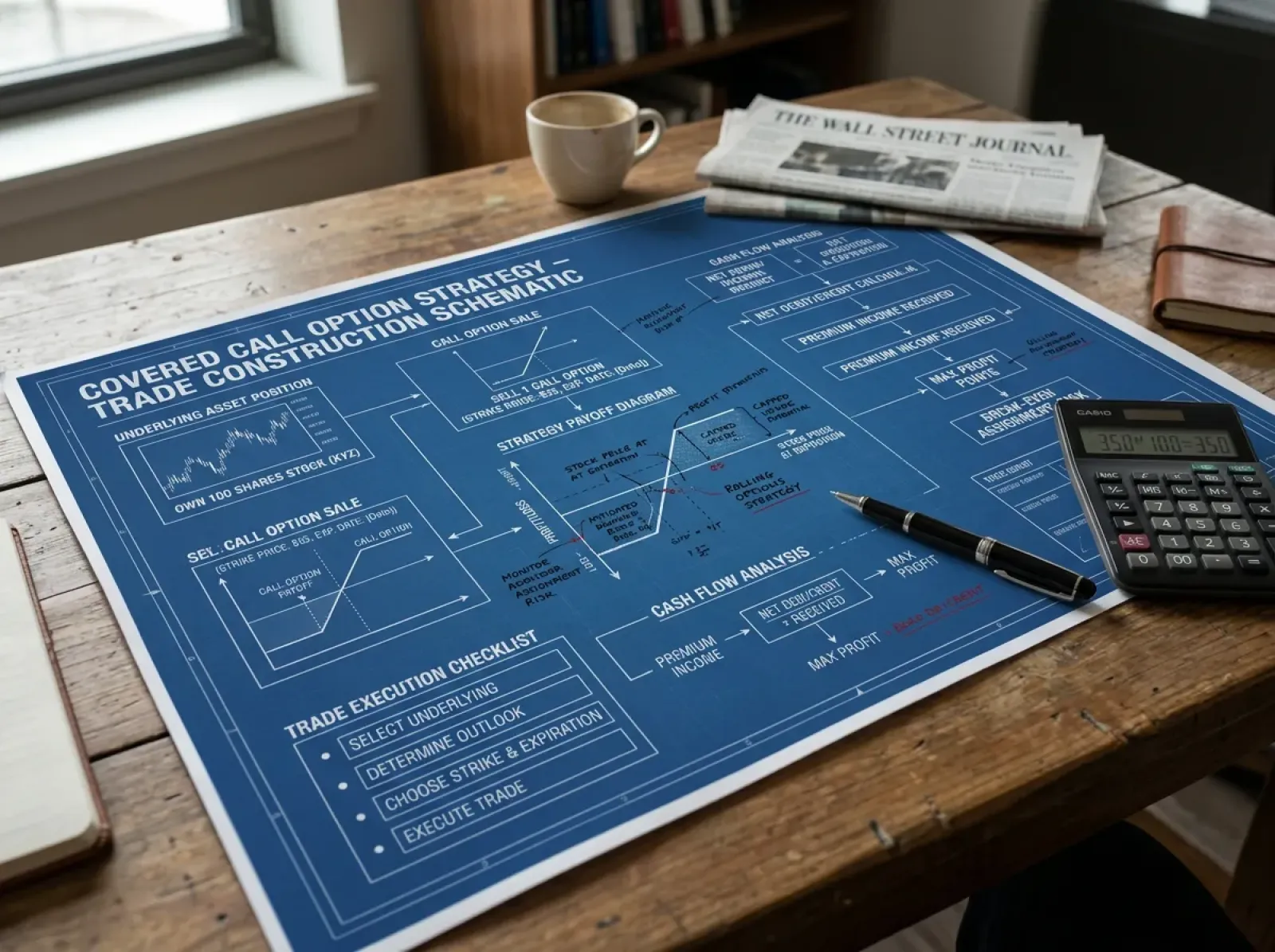

Anatomy of a Covered Call Trade

Every covered call trade requires three decisions: which stock to use, which strike price to sell, and which expiration date to choose. These decisions interact with each other and collectively determine your potential income, your probability of assignment, and your risk-reward profile. Getting comfortable with this decision framework transforms the covered call strategy from an abstract concept into a practical tool you can apply repeatedly across your portfolio.

Components of structuring a covered call:

-

The underlying stock must be one you own in lots of at least 100 shares, since each option contract represents 100 shares

-

You should be comfortable potentially selling these shares at the strike price you select

-

The strike price determines both how much premium you receive and how likely assignment becomes

-

Higher strike prices mean less premium but more room for upside before assignment

-

Lower strike prices mean more premium but higher probability of losing your shares

-

The expiration date determines how long your obligation lasts and how much time value exists in the premium

-

Longer expirations generally offer more total premium but tie up your position for extended periods

-

Shorter expirations offer less premium per trade but allow more frequent adjustment and decision-making

-

Implied volatility of the underlying stock affects premium levels—higher volatility means richer premiums

-

Dividend dates matter because calls may be exercised early to capture dividends, affecting your planning

Calculating Potential Outcomes

Before entering any covered call, you should know exactly what happens in each scenario—stock up, stock flat, stock down—so nothing surprises you.

The math is straightforward once you understand the components. Your maximum profit equals the difference between the strike price and your cost basis, plus the premium received. This maximum occurs when the stock rises to exactly the strike price or higher at expiration. If you bought shares at $50, sold a $55 strike call for $2 premium, your maximum profit is $7 per share ($5 stock gain plus $2 premium). Your breakeven point equals your cost basis minus the premium received—in this example, $48. Below $48, you're losing money on the overall position despite keeping the premium. If the stock stays flat at $50, you profit by the $2 premium alone, a 4% return for the period of the trade. If the stock drops to $45, your shares show a $5 loss, but the $2 premium reduces your net loss to $3 per share. Running these calculations before every trade clarifies exactly what you're agreeing to and helps you select appropriate strike prices and expirations for your outlook.

Keep In Mind: The covered call strategy requires upfront clarity on three decisions—stock selection, strike price, and expiration date—and running the math on potential outcomes before entering ensures you understand your maximum profit, breakeven point, and downside exposure rather than discovering these realities after the trade is on.

Strike Price Selection Strategies

Strike price selection is the most consequential decision in the covered call strategy because it determines the balance between income and upside potential. A lower strike generates more premium but increases the likelihood of assignment and caps your gains at a lower level. A higher strike generates less premium but gives the stock more room to appreciate before you're obligated to sell. There's no universally correct answer—the right strike depends on your market outlook, your income goals, and how attached you are to keeping your shares.

At-the-Money and In-the-Money Strikes

At-the-money calls have strike prices equal to or very close to the current stock price, while in-the-money calls have strikes below the current price—both generate substantial premium but limit upside significantly.

At-the-money strikes offer the highest time value premium because uncertainty about whether the option finishes in or out of the money is maximized. If your stock trades at $50 and you sell the $50 strike call, you're collecting maximum time premium but capping your gains at the current price. In-the-money strikes go further—selling a $47.50 call when the stock is at $50 generates even more total premium (including $2.50 of intrinsic value) but means you're already committed to selling below the current price if held to expiration. These aggressive approaches make sense when you're neutral to slightly bearish, want maximum downside protection from premium, or are comfortable exiting the position at current or lower prices.

DO use at-the-money strikes when you want maximum time premium and believe the stock will trade sideways.

DO consider in-the-money strikes when you want significant downside protection and are ready to exit the position.

DO recognize that higher premium comes with higher assignment probability—you're being paid more because you're giving up more.

DON'T sell at-the-money or in-the-money calls on stocks you strongly believe will appreciate significantly.

DON'T ignore that in-the-money calls have very high assignment probability, especially approaching expiration.

DON'T use these aggressive strikes if being called away would cause regret or tax complications you're not prepared for.

Out-of-the-Money Strikes

Out-of-the-money calls have strike prices above the current stock price, offering less premium but more room for appreciation before assignment becomes likely.

This approach suits investors who want to participate in moderate upside while still collecting some income. If your stock trades at $50 and you sell the $55 strike call, you're giving the position room to appreciate 10% before your shares get called away. The trade-off is less premium—out-of-the-money options consist entirely of time value with no intrinsic value, and that time value decreases as the strike moves further from the current price.

How to match out-of-the-money strike selection to your outlook:

-

Slightly out-of-the-money strikes (2-3% above current price) balance meaningful premium with modest upside participation

-

Moderately out-of-the-money strikes (5-7% above current price) prioritize upside participation while still generating income

-

Far out-of-the-money strikes (10%+ above current price) generate minimal premium but rarely result in assignment

-

Higher implied volatility environments make out-of-the-money strikes more attractive because premiums are elevated across all strikes

-

Earnings announcements and other events inflate out-of-the-money premiums, creating opportunities for those who want upside exposure

-

Your willingness to be assigned should guide strike selection—choose strikes where selling at that price would feel acceptable, not painful

-

If you're using covered calls primarily for income, strikes closer to the money make sense despite higher assignment risk

-

If you're using covered calls to slightly enhance returns while maintaining most upside exposure, further out-of-the-money strikes fit better

Remember: Strike price selection in the covered call strategy reflects your market outlook and priorities—at-the-money and in-the-money strikes maximize premium but cap gains immediately, while out-of-the-money strikes sacrifice premium for upside participation, and the right choice depends on whether you prioritize income or appreciation potential for each specific position.

Expiration Date Considerations

Expiration date selection determines how long you're committed to the covered call position and significantly affects the premium you receive. Options lose value over time as expiration approaches—a phenomenon called time decay or theta—and this decay accelerates in the final weeks before expiration. Understanding how time decay works helps you choose expirations that match your income goals, management preferences, and outlook on how long the stock will remain in your desired trading range.

Factors to weigh when selecting expiration dates:

-

Weekly options (expiring within 7 days) offer the fastest time decay and most frequent trading opportunities but generate the least total premium per trade

-

Monthly options (expiring in 30-45 days) represent the traditional sweet spot, balancing meaningful premium with manageable time commitment

-

Longer-dated options (60-90+ days) generate more total premium but tie up your position and expose you to more potential stock movement

-

Time decay accelerates dramatically in the final 30 days before expiration, with the steepest decay occurring in the last two weeks

-

Selling 30-45 day options captures this acceleration while still collecting reasonable premium

-

Shorter expirations require more active management and generate more transaction costs from frequent trading

-

Longer expirations reduce trading frequency but give the stock more time to move against your position

-

Implied volatility affects all expirations but has proportionally larger impact on longer-dated options

-

Earnings dates, dividends, and other scheduled events create premium spikes that affect certain expirations more than others

-

Your available time for monitoring positions should influence expiration choice—weekly options demand attention, quarterly options allow passivity

-

The covered call strategy works across all expiration timeframes, but your choice should reflect your management style and income objectives

Time Decay and Its Effect on Premium

Time decay is the covered call seller's best friend—it works in your favor every day, eroding the value of the option you sold and increasing the likelihood you keep the full premium.

Options have two components of value: intrinsic value (how much they're in the money) and time value (premium for the possibility of favorable movement before expiration). Time value decays to zero by expiration. As a call seller, you've received this time value upfront, and every day that passes with the stock below your strike means that value transfers from the option buyer to you. The decay isn't linear—it accelerates as expiration approaches following a curve that steepens dramatically in the final weeks.

How time decay affects covered call management:

-

Options lose roughly one-third of their time value in the first half of their life and two-thirds in the second half

-

The final two weeks before expiration see the fastest decay, making this period most favorable for sellers

-

Selling 30-45 day options lets you capture this acceleration zone while still receiving meaningful premium

-

If your option has lost 70-80% of its value with time remaining, buying it back early locks in most of your profit and frees you to sell another

-

Rolling to a new expiration before the final week means giving up some of the steepest decay—a trade-off between management flexibility and maximum decay capture

-

Low volatility environments slow time decay's impact because there's less time value to decay in the first place

-

High volatility environments accelerate the absolute dollar amount of decay even though the percentage rate follows the same curve

Think of it this way: Time decay in the covered call strategy works like a melting ice cube—it happens slowly at first, then rapidly accelerates as expiration approaches, and as the seller who received premium upfront, you benefit from every drop that melts away because it represents value you've already pocketed that the buyer can never recover.

Calculating Returns and Breakeven

The math behind covered calls is refreshingly straightforward, which is part of what makes the strategy accessible to investors who might otherwise avoid options. Before entering any covered call position, you should be able to calculate exactly how much you can make, where your breakeven sits, and what returns look like on an annualized basis. These calculations remove uncertainty from the equation and let you evaluate whether a particular trade meets your income objectives before committing capital.

Maximum Profit and Breakeven

Every covered call has a defined maximum profit and a clear breakeven point—knowing both before you trade ensures you're entering with realistic expectations.

The maximum profit occurs when the stock rises to exactly the strike price or higher at expiration. At that point, you capture all the premium plus any stock appreciation up to the strike. The breakeven point represents the stock price below which you begin losing money on the overall position, accounting for the premium cushion you've received.

Step one: Identify your cost basis in the stock. This is what you paid per share, or your adjusted basis if you've held the position for some time. For this example, assume you bought 100 shares at $50 per share.

Step two: Identify the call option you're selling. Assume you sell one $55 strike call expiring in 45 days for $2.00 per share ($200 total premium for the contract).

Step three: Calculate your maximum profit. Maximum profit equals the strike price minus your cost basis, plus the premium received. In this case: ($55 - $50) + $2 = $7 per share, or $700 total. This occurs if the stock is at $55 or higher at expiration.

Step four: Calculate your breakeven point. Breakeven equals your cost basis minus the premium received. In this case: $50 - $2 = $48. Below $48, you're losing money on the combined position despite keeping the premium.

Step five: Calculate your static return if the stock stays flat. If the stock remains at $50, your return is simply the premium divided by your cost basis: $2 / $50 = 4% for the 45-day period.

Step six: Calculate your maximum return. Maximum return equals maximum profit divided by cost basis: $7 / $50 = 14% for the 45-day period, achieved if assigned at the $55 strike.

Annualized Return Considerations

Single-trade returns tell only part of the story—annualizing those returns helps you compare covered call income to other investment approaches and set realistic portfolio expectations.

The covered call strategy generates returns over specific time periods that don't align with annual reporting conventions. A 4% return over 45 days sounds modest until you annualize it. Converting period returns to annual equivalents requires accounting for how many times you could theoretically repeat the trade in a year.

How to think about annualized returns:

-

Annualized return equals period return multiplied by (365 divided by days in the trade)

-

A 4% return over 45 days annualizes to approximately 32% (4% × 365/45)

-

A 2% return over 30 days annualizes to approximately 24% (2% × 365/30)

-

A 1% return over 7 days annualizes to approximately 52% (1% × 365/7)

-

These annualized figures assume you can repeat the trade continuously at similar returns, which rarely happens perfectly

-

Assignment, stock movement, and changing volatility all affect whether annualized projections match reality

-

Transaction costs reduce actual returns, particularly for frequent weekly trading strategies

-

Annualized returns help compare opportunities but shouldn't be treated as guaranteed outcomes

-

A realistic covered call program on stable, moderately volatile stocks might generate 8-15% annualized income in normal conditions

-

High annualized return projections often indicate either very short timeframes or elevated risk that may not be sustainable

-

Comparing annualized covered call returns to dividend yields or bond yields provides useful context for income-focused portfolios

When Covered Calls Work Best

The covered call strategy isn't a one-size-fits-all solution—it thrives under specific conditions and struggles under others. Understanding when the strategy has tailwinds behind it helps you deploy it selectively rather than mechanically applying it across your entire portfolio regardless of circumstances. The ideal covered call environment combines the right market outlook, favorable volatility conditions, appropriate underlying stocks, and psychological readiness to accept assignment.

Conditions that favor covered call performance:

-

Neutral to slightly bullish market outlook where you expect the stock to trade sideways or drift modestly higher but not surge

-

You believe the stock is fairly valued and unlikely to make large moves in either direction over the option's timeframe

-

High implied volatility environments where option premiums are elevated relative to historical norms, meaning you're paid more for the same obligation

-

Volatility spikes from market uncertainty or sector-specific concerns that inflate premiums without necessarily reflecting the stock's actual likely movement

-

Stocks with liquid options markets where tight bid-ask spreads reduce transaction costs and allow efficient entry and exit

-

Large-cap, well-known stocks with active options trading rather than small-caps with wide spreads and limited strike availability

-

Positions you've held for gains and would be comfortable selling at a profit if assigned at the strike price

-

Stocks where assignment wouldn't trigger unwanted tax consequences or disrupt your broader portfolio strategy

-

Dividend-paying holdings where covered calls add a second income stream on top of the dividend yield

-

Stocks approaching ex-dividend dates where call premiums often increase slightly to account for the dividend

-

Shares you own but don't expect to outperform significantly over the near term, making income enhancement attractive

-

Portfolio positions that have become oversized where assignment would actually help with rebalancing

-

Retirement accounts where tax implications of assignment are less complex

-

Market environments where you want downside cushioning from premium received even if the stock declines moderately

-

Periods when you have time to monitor positions and manage them actively if needed

The Ideal Covered Call Candidate

The perfect covered call scenario combines several favorable factors simultaneously, though you'll rarely find every element aligned perfectly.

The covered call strategy works best on a moderately volatile stock you own at a comfortable cost basis, in an environment where implied volatility has spiked above historical averages, when your outlook suggests sideways to modestly higher movement over the coming weeks, and when you'd be genuinely content to sell shares at your chosen strike price if the market moves against you. Finding stocks that check most of these boxes—rather than forcing covered calls onto positions that don't fit—dramatically improves your results over time.

When Covered Calls Struggle

Just as certain conditions favor covered calls, other environments work against them or create frustrations that outweigh the income benefits. Recognizing when not to deploy the strategy saves you from trades that generate modest premiums while exposing you to regret, missed opportunities, or losses that exceed what you collected. The covered call strategy has real limitations, and pretending otherwise leads to disappointment.

Conditions that work against covered call performance:

-

Strongly bullish trending markets where stocks consistently exceed strike prices, leading to repeated assignment and missed upside

-

Periods when your holdings are likely to appreciate significantly, making the premium received feel trivial compared to gains forfeited

-

Low implied volatility environments where premiums are depressed and barely worth the effort and transaction costs

-

Calm market conditions where option prices reflect minimal expected movement, reducing income potential across all strikes

-

Stocks approaching earnings announcements, FDA decisions, or other binary events where large moves in either direction are likely

-

Situations where assignment would trigger short-term capital gains on shares you've held for nearly a year

-

Holdings where your cost basis is underwater and assignment would lock in losses rather than gains

-

Stocks you're deeply attached to emotionally and would feel genuine regret about selling at any price

-

Positions in companies you believe in long-term where capping upside conflicts with your investment thesis

-

Illiquid options markets where wide bid-ask spreads eat into premium and make adjustments expensive

-

Small positions where the premium collected barely covers commission costs and management effort

-

Volatile stocks where downside risk exceeds the protective cushion that modest premiums provide

-

Periods when you can't actively monitor positions and might miss management opportunities

-

Tax situations where generating short-term income creates complications that outweigh the premium benefits

-

Holdings you've inherited or received as gifts where the cost basis situation makes assignment problematic

The Emotional Attachment Problem

One of the most common covered call mistakes involves selling calls on shares you don't actually want to part with, then experiencing regret or panic when assignment becomes likely.

The strategy requires genuine willingness to sell at your chosen strike price. Intellectual acceptance isn't enough—you need emotional readiness. Many investors sell calls thinking assignment is unlikely, then watch helplessly as the stock rallies past their strike. The premium that seemed attractive becomes trivial compared to the gains they're about to miss. Some buy back calls at losses to avoid assignment, then watch the stock pull back, meaning they paid to avoid losing shares they would have kept anyway. Others accept assignment with lingering resentment that colors their view of the strategy forever.

DO evaluate honestly whether you'd truly be comfortable selling at the strike price before entering any covered call.

DO recognize that some stocks in your portfolio aren't appropriate covered call candidates regardless of premium available.

DO accept that assignment is a feature of the strategy, not a failure—if you selected appropriate strikes, you're selling at a price you were comfortable with.

DON'T sell calls on positions you consider long-term core holdings that you'd regret losing.

DON'T assume you can always roll out of assignment risk—sometimes the stock runs far enough that rolling becomes impractical or expensive.

DON'T let greed for premium override honest assessment of your attachment to specific holdings.

The Bottom Line: The covered call strategy struggles in strongly trending markets where you repeatedly miss upside, low volatility environments where premiums don't justify the effort, around binary events that create unpredictable large moves, and most importantly on shares you're emotionally attached to—recognizing these limitations helps you deploy covered calls selectively on appropriate positions rather than generating regret by forcing the strategy where it doesn't belong.

Managing Covered Call Positions

Entering a covered call is only half the equation—managing the position through expiration requires understanding your options (literally) as the trade develops. The covered call strategy doesn't demand constant attention, but knowing how to respond when stocks move significantly in either direction separates experienced practitioners from beginners who simply hope for the best. Four basic outcomes exist, and each offers different management choices depending on your goals and market view.

Management scenarios and responses:

-

Stock stays below strike through expiration: the call expires worthless, you keep shares and full premium, and you can immediately sell another call to continue generating income

-

Stock rises above strike near expiration: assignment becomes likely, and you must decide whether to accept selling your shares or take action to avoid assignment

-

Stock drops significantly: the call expires worthless, but you're sitting on unrealized losses offset partially by premium received

-

Stock rises modestly but stays near the strike: the call may or may not be assigned depending on exactly where the stock closes, creating uncertainty into expiration

-

Rolling out means buying back your current call and selling a new call at a later expiration, extending your time horizon while potentially collecting additional premium

-

Rolling up means buying back your current call and selling a new call at a higher strike price, giving the stock more room to appreciate at the cost of some premium

-

Rolling up and out combines both moves, selecting a higher strike at a later expiration, often used when the stock has rallied and you want to avoid assignment

-

Rolling down means buying back your current call and selling a new call at a lower strike, typically done after a stock decline to collect more premium and lower your breakeven

-

Buying back calls early captures most of your profit before expiration if the option has lost significant value, freeing you to sell another call immediately

Rolling Strategies and Early Buyback

Rolling and early buyback represent active management techniques that let you adapt to changing conditions rather than passively waiting for expiration.

When a stock moves against your position—either rising toward your strike or falling significantly—rolling offers a way to adjust without simply accepting the original outcome. If your stock has rallied and you don't want assignment, buying back the current call (at a loss) and selling a new call at a higher strike and/or later date can defer assignment while potentially breaking even or collecting additional net premium. The trade-off is that you're extending your commitment and may need the stock to cooperate over a longer period. Early buyback makes sense when your call has lost 70-80% of its value with meaningful time remaining. At that point, most of your potential profit is captured, and buying back the call lets you sell a fresh position immediately rather than waiting for the final 20-30% of decay that might take weeks to materialize.

Quick tip: Set a target to buy back calls when they've lost 50-80% of their initial value—this captures most of your profit while freeing capital to establish new positions rather than waiting for diminishing returns.

Quick tip: When rolling to avoid assignment, evaluate whether the net credit received justifies extending your commitment—sometimes accepting assignment and moving on makes more sense than rolling into an unattractive new position.

Did You Know? Early assignment on covered calls is relatively rare except when a stock is deep in the money and approaching an ex-dividend date, because call buyers generally prefer to sell their options rather than exercise them and lose remaining time value.

Did You Know? Many covered call practitioners establish their positions with a predetermined management plan—such as "buy back at 50% profit or roll if stock exceeds strike by 3%"—removing emotion from real-time decisions and creating a systematic approach to the covered call strategy.

Common Covered Call Mistakes

The covered call strategy is straightforward in concept but offers plenty of opportunities for self-sabotage in practice. Most mistakes fall into predictable categories that experienced traders learn to avoid—often after making them at least once. Understanding these pitfalls before you encounter them accelerates your learning curve and protects your returns from errors that seem obvious in hindsight but feel tempting in the moment.

Common mistakes that erode covered call returns:

-

Selling calls on stocks you genuinely don't want to sell, then experiencing regret, panic, or expensive rolling when assignment approaches

-

Choosing strike prices based purely on premium size without honestly evaluating whether you'd accept assignment at that level

-

Chasing high premiums by selling calls on volatile, speculative stocks where the underlying position risk far exceeds the income benefit

-

Treating elevated premium as free money rather than recognizing it reflects genuine risk the market is pricing into the option

-

Buying risky stocks specifically to write covered calls against them, reversing the proper logic of the strategy

-

Ignoring ex-dividend dates when calls may be exercised early to capture dividends, leading to unexpected assignment

-

Selling calls just before ex-dividend dates without understanding that in-the-money calls face elevated early assignment risk

-

Failing to account for dividends when calculating your total return from covered call positions

-

Over-trading by rolling positions constantly or selling weekly options when the premium barely covers transaction costs

-

Letting trading frequency create tax complications and commission drag that overwhelm the income generated

-

Selling calls with expirations too short to generate meaningful premium after bid-ask spreads and commissions

-

Focusing exclusively on annualized return projections that assume perfect repeatability when reality involves gaps, assignment, and adjustment costs

-

Neglecting position sizing by writing calls against your entire stock position when keeping some shares uncovered would provide upside exposure

-

Failing to track cost basis and premium received, making it difficult to evaluate actual returns or manage tax implications

-

Entering covered calls without a management plan, leading to emotional decisions when the stock moves significantly

-

Selling calls during low volatility periods when premiums are depressed rather than waiting for better entry points

-

Ignoring upcoming events like earnings announcements that could cause large moves in either direction

-

Treating assignment as failure rather than a planned outcome that you should have been comfortable with when entering the trade

-

Comparing covered call returns to buy-and-hold returns in hindsight rather than evaluating the strategy based on your actual outlook at entry

-

Abandoning the strategy after one bad experience rather than recognizing that individual trades vary while the approach works over time

Think of it this way: The covered call strategy fails most often not from market conditions but from human error—selling calls on shares you secretly hope won't be called away, chasing premium without respecting underlying risk, ignoring the calendar, and letting transaction costs consume your income through excessive trading—and avoiding these mistakes matters more than optimizing strike selection or timing.

Making the Covered Call Strategy Your Own

The covered call strategy offers something genuinely useful for stock investors: a structured way to generate income from existing holdings while maintaining most of the benefits of stock ownership. You collect premium immediately, reduce your cost basis over time, and create a systematic approach to monetizing positions that might otherwise sit passively in your portfolio. The trade-off—capping your upside in exchange for immediate income—isn't right for every position or every market environment, but for appropriate holdings in suitable conditions, covered calls transform the waiting game of investing into an active income-generating process.

Building Your Covered Call Practice

Success with covered calls comes from accumulated experience, realistic expectations, and gradual refinement of your approach rather than searching for perfect trades.

Start with positions you genuinely wouldn't mind selling, select conservative out-of-the-money strikes that give stocks room to appreciate, and choose monthly expirations that balance premium with manageable time commitment. Track your results honestly, including trades where you missed upside or where the stock declined more than your premium cushioned. Over time, you'll develop intuition for which holdings make good covered call candidates, which volatility environments favor the strategy, and how aggressive to be with strike selection based on your outlook. Realistic income expectations matter—annualized returns of 6-12% on stable, moderately volatile positions represent solid covered call performance, while projections of 20%+ usually indicate either elevated risk or calculation optimism. The covered call strategy works best as one component of a broader portfolio approach, applied selectively to appropriate positions rather than mechanically across everything you own. Give yourself permission to leave some shares uncovered when you're bullish, and recognize that the strategy's value compounds over years of consistent application rather than manifesting in any single trade.