Understanding the Carry Trade Strategy

The carry trade is one of the oldest and most widely used strategies in currency markets, built on a simple concept: borrow money in a currency with low interest rates, convert it to a currency with high interest rates, and pocket the difference. As long as the exchange rate doesn't move against you by more than you earn in interest, you profit. The strategy appeals to traders and institutions alike because it generates returns simply from holding a position, collecting interest payments day after day regardless of whether the currency pair moves in your favor. When conditions align—stable exchange rates, predictable central bank policies, and meaningful interest rate differentials—carry trades can produce consistent income that compounds over time.

Why Interest Rate Differentials Create Opportunity

Interest rates differ between countries because central banks set monetary policy based on domestic economic conditions, inflation pressures, and growth objectives. When Japan keeps rates near zero to stimulate its economy while the United States maintains rates at 5% to combat inflation, that 5% gap creates an arbitrage-like opportunity. Traders who borrow yen at near-zero cost and hold dollars earning 5% capture that spread. The opportunity exists because currency markets don't immediately price in future interest rate changes perfectly, and because many market participants have mandates, constraints, or objectives that prevent them from pursuing pure carry strategies even when they appear attractive.

What This Article Covers

The carry trade strategy sounds straightforward but involves subtleties and risks that determine whether it generates steady income or devastating losses.

Topics this article will explain:

-

How the carry trade works mechanically, including borrowing, converting, and earning the interest differential

-

The history of carry trading from the Japanese yen carry boom through the 2008 crisis and beyond

-

Popular currency pairs used for carry trades and how to identify attractive opportunities

-

Calculating carry trade returns including swap rates, rollover, and realistic yield expectations

-

The significant risks of carry trading, particularly currency depreciation and sudden risk-off unwinds

-

Market conditions when carry trades work best and when they fail catastrophically

-

Managing carry trade positions through proper sizing, stops, and ongoing monitoring

The Bottom Line: The carry trade strategy profits from interest rate differentials between currencies, earning yield simply from holding positions, but understanding when conditions favor the strategy and when they threaten sudden reversals separates profitable carry traders from those who learn expensive lessons about how quickly currency moves can erase months of accumulated interest.

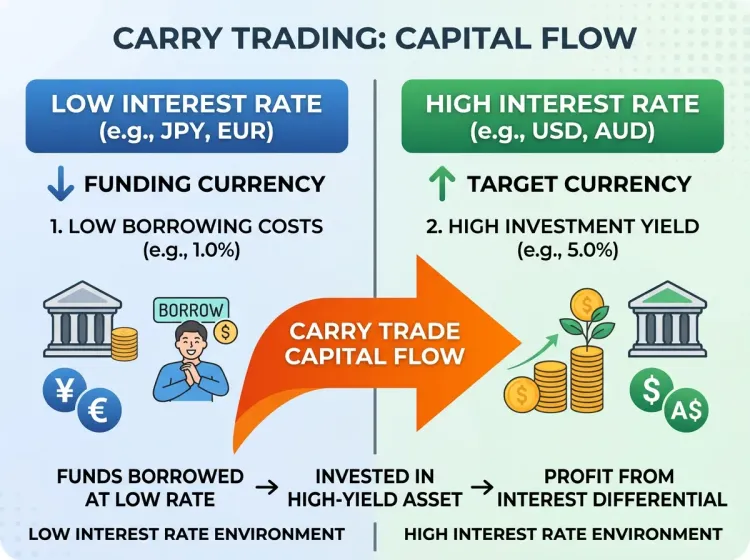

How the Carry Trade Works

The carry trade exploits the fact that different currencies offer different interest rates, creating an opportunity to profit from the spread between them. In its simplest form, you borrow money in a currency where interest rates are low, convert that money into a currency where interest rates are high, and earn the difference between what you pay and what you receive. The strategy works in forex markets because when you trade currency pairs, you're simultaneously buying one currency and selling another—effectively going long the high-yielding currency while shorting the low-yielding one. Each day you hold the position, your broker credits or debits your account based on the interest rate differential, a process called rollover or swap.

How the carry trade generates returns:

-

Borrow or sell a currency with low interest rates, often called the funding currency

-

Buy or invest in a currency with high interest rates, called the target currency

-

Hold the position overnight to earn the interest rate differential credited through daily rollover

-

Accumulate interest payments that compound over time as long as the position remains open

-

Profit from both the carry (interest) and any favorable exchange rate movement if the target currency appreciates

-

The trade remains profitable as long as exchange rate losses don't exceed accumulated interest income

-

Leverage amplifies the interest earned relative to capital deployed, magnifying both potential returns and risks

The Role of Leverage

Leverage transforms the carry trade from a modest yield strategy into something with substantial return potential—but also substantial risk.

Without leverage, the carry trade offers returns roughly equal to the interest rate differential, perhaps 3-5% annually in favorable conditions. This resembles bond yields more than trading profits. But forex markets offer significant leverage, often 20:1 or higher for retail traders and far greater for institutions. If you control $100,000 in currency with $5,000 in capital and earn 4% annual carry, your return on actual capital deployed is 80% before accounting for exchange rate movements. This leverage effect explains why carry trades attract so much capital when conditions appear stable. It also explains why carry trade unwinds can be so violent—the same leverage that amplifies interest income amplifies currency losses when positions move against traders.

Basic Mechanics in Practice

Understanding how the carry trade works in actual forex trading clarifies what happens in your account and what you're actually paying and receiving.

The practical mechanics of carry trading:

-

When you go long a currency pair, you're buying the base currency and selling the quote currency

-

If the base currency has the higher interest rate, you receive positive carry; if the quote currency is higher, you pay negative carry

-

Rollover occurs at 5pm Eastern time when positions are carried to the next trading day

-

Your broker calculates the swap rate based on the interbank interest differential minus their markup

-

Wednesday rollovers typically include triple swap to account for the weekend when markets are closed

-

Swap rates appear in your trading platform and can differ significantly between brokers

-

The actual swap you receive is usually less than the theoretical interest rate differential due to broker spreads and costs

-

Positive carry accumulates in your account balance daily, compounding over weeks and months if the position remains open

The History of Carry Trading

The carry trade has existed as long as interest rate differentials between countries have existed, but it became a dominant force in currency markets during the 1990s and 2000s when Japan's persistent near-zero interest rates created the perfect funding currency. For over two decades, traders could borrow yen at essentially no cost and invest in virtually any other currency for a positive spread. This wasn't a niche strategy—it became one of the largest and most crowded trades in global finance, with estimates suggesting hundreds of billions of dollars deployed in yen-funded carry positions at peak levels. Understanding this history helps explain both the strategy's appeal and its dangers.

The Japanese Yen as the Classic Funding Currency

Japan's unique economic circumstances made the yen the world's go-to currency for funding carry trades for decades.

Why the yen dominated carry trade funding:

-

Japan's central bank maintained near-zero interest rates from the mid-1990s through the 2020s to combat deflation and stimulate growth

-

The yen offered deep liquidity and easy convertibility, making large positions practical to establish and exit

-

Japanese economic stability meant the funding currency was unlikely to spike in value due to domestic crises

-

The interest rate gap between Japan and higher-yielding countries like Australia, New Zealand, and emerging markets created attractive spreads

-

Institutional investors, hedge funds, and retail traders all participated in yen-funded carry trades simultaneously

-

The trade became so crowded that it created self-reinforcing dynamics—carry inflows weakened the yen further, boosting returns

-

At peak periods before 2008, yen carry trades represented one of the most consensus positions in global macro trading

The 2008 Crisis and Carry Trade Unwinding

The 2008 financial crisis demonstrated what happens when a crowded carry trade unwinds violently and simultaneously.

IF global risk appetite suddenly collapses due to a financial crisis or major shock event… THEN carry traders rush to exit positions simultaneously, buying back the funding currency they shorted.

IF everyone who borrowed yen to fund carry trades suddenly needs to buy yen to close positions… THEN the yen surges in value as demand overwhelms available supply.

IF the yen appreciates rapidly while traders hold short yen positions… THEN currency losses quickly exceed accumulated carry income, turning profitable trades into substantial losses.

IF leverage amplified the carry trade returns during the good times… THEN that same leverage amplifies losses during the unwind, potentially exceeding total account equity.

IF the unwind happens faster than traders can exit positions… THEN liquidity evaporates, spreads widen dramatically, and stop losses execute at far worse prices than intended.

IF institutional carry traders face margin calls during the unwind… THEN forced liquidation creates additional selling pressure, accelerating the cascade in a destructive feedback loop.

Recent Evolution and Current Landscape

The carry trade landscape has shifted dramatically since 2008, with new funding currencies emerging and interest rate differentials changing across multiple cycles.

The post-2008 environment initially crushed carry trade opportunities as central banks globally slashed rates toward zero, eliminating differentials. The yen remained a funding currency, but target currencies offered diminishing yields. Then came the post-pandemic inflation surge that created new dynamics—the Federal Reserve raised rates aggressively while Japan maintained ultra-low rates, widening the USD/JPY differential to levels not seen in decades. By 2023-2024, the yen carry trade had returned with force, with the currency weakening to multi-decade lows against the dollar. But the strategy's history offers a cautionary lesson: the most profitable carry environments often precede the most violent unwinds. When everyone sees the same opportunity and crowds into the same trade, the eventual exit becomes a stampede rather than an orderly retreat.

Popular Carry Trade Currency Pairs

Not all currency pairs work equally well for carry trading. The ideal carry pair combines a meaningful interest rate differential with reasonable exchange rate stability and sufficient liquidity to enter and exit positions without excessive slippage. Some pairs have become classics in the carry trading world, returning to favor whenever rate differentials widen. Others offer higher yields but come with volatility and liquidity risks that can quickly erase carry income. Understanding which pairs traders commonly use—and why—helps you evaluate opportunities when interest rate environments create attractive conditions.

Popular currency pairs for carry trading:

-

USD/JPY remains the dominant carry pair when US rates exceed Japanese rates, offering deep liquidity, tight spreads, and a persistent differential that has existed for decades

-

AUD/JPY combines Australian commodity currency exposure with yen funding, historically offering attractive carry when Australian rates exceed Japan's near-zero policy

-

NZD/JPY follows similar logic to AUD/JPY with New Zealand's historically higher rates funded by borrowed yen

-

EUR/JPY provides carry opportunities when European rates exceed Japanese rates, though differentials have been smaller historically

-

MXN/JPY offers higher yields through Mexican peso exposure but introduces emerging market volatility and political risk

-

ZAR/JPY targets South African rand yields but carries significant risk from rand volatility and South African economic instability

-

TRY/JPY and other Turkish lira pairs have offered extremely high nominal yields but currency depreciation has historically wiped out carry gains

-

USD/CHF can work when US rates significantly exceed Swiss rates, with the franc serving as an alternative funding currency to the yen

-

Emerging market pairs against low-rate currencies offer high nominal yields but require careful risk assessment

How to Identify Attractive Carry Pairs

Finding good carry trade opportunities requires looking beyond simple interest rate differentials to evaluate the complete risk-reward picture.

DO start by checking current central bank policy rates for both currencies in any pair you're considering.

DO verify actual swap rates at your broker, since theoretical differentials don't equal what you'll actually receive after broker markups.

DO evaluate historical volatility of the pair to understand how much exchange rate risk you're taking for the carry you'll receive.

DO consider the macroeconomic stability of both countries, since political or economic crises can cause rapid currency moves that dwarf carry income.

DO assess liquidity by checking spreads and trading volume, particularly if you plan to hold large positions or need quick exits.

DO monitor central bank communication for hints about future rate changes that could narrow or widen the differential.

DO look at the trend direction—carry trades work better when the high-yield currency is also appreciating or at least stable.

DON'T chase the highest yields without considering why those yields are so high—extreme rates often reflect extreme risk.

DON'T assume historical carry relationships will persist—central bank policies change and differentials narrow or reverse.

DON'T ignore emerging market risks including capital controls, currency crises, and liquidity evaporation during stress.

DON'T overlook that your broker's swap rates can change without notice as interbank rates fluctuate.

DON'T enter carry trades in pairs where the high-yield currency is already in a downtrend, as depreciation will likely exceed carry income.

Remember: Popular carry trade currency pairs like USD/JPY, AUD/JPY, and emerging market crosses against low-rate funding currencies offer different combinations of yield and risk, and identifying attractive opportunities requires evaluating not just the interest rate differential but also volatility, liquidity, trend direction, and the macroeconomic stability of both countries involved.

Calculating Carry Trade Returns

Understanding exactly how much you'll earn from a carry trade requires moving beyond theoretical interest rate differentials to the practical reality of what your broker actually pays. The difference between central bank policy rates and the swap rates credited to your account can be substantial, and this gap directly affects your expected returns. Calculating realistic carry returns before entering positions helps you evaluate whether the yield justifies the exchange rate risk you're taking—and prevents disappointment when your actual earnings fall short of what simple rate comparisons might suggest.

Understanding Swap Rates and Rollover

Swap rates represent the actual interest differential you receive or pay when holding positions overnight, and they differ from simple policy rate comparisons.

How brokers calculate overnight interest:

Brokers determine swap rates based on the interbank lending rates for each currency, typically derived from benchmarks like SOFR, EONIA, or TIBOR rather than central bank policy rates directly. They calculate the theoretical interest differential between the two currencies in the pair, then adjust for their own costs and profit margin. The resulting swap rate is expressed as either points or a cash amount per lot per night. When you hold a position past the daily rollover time (typically 5pm Eastern), your account is credited for positive carry or debited for negative carry based on these swap rates. Wednesday rollovers usually include triple swap to account for the weekend settlement period. Your broker publishes current swap rates on their platform, though these rates can change daily as underlying interbank rates fluctuate.

Positive vs. Negative Carry

The direction of your position determines whether you earn or pay the interest differential, and getting this wrong turns a carry strategy into a carry cost.

When you go long a currency pair, you're buying the base currency and selling the quote currency. If the base currency has the higher interest rate, you earn positive carry—interest credited to your account each night you hold. If the quote currency has the higher rate, you pay negative carry—interest debited from your account. Going short reverses this relationship. The same pair can offer positive or negative carry depending on whether you're long or short. Traders seeking carry income must position in the direction that earns rather than pays the differential, which sometimes conflicts with technical or fundamental directional views.

Annualized Carry Calculations

Converting nightly swap payments into annualized returns helps you compare carry trade yields to other investment opportunities.

Quick tip: Multiply your nightly swap payment by 365 to get annual carry income, then divide by your margin requirement to calculate return on capital deployed—this reveals your leveraged yield.

Quick tip: Check your broker's swap rates against competitors, as differences between brokers can meaningfully impact your annualized returns on the same trade.

Did You Know? The swap rate you receive is typically 0.5% to 1.5% lower than the theoretical interest rate differential would suggest, as brokers capture this spread as profit for facilitating the rollover process.

Realistic Return Expectations

The carry trade strategy generates modest unleveraged returns that leverage transforms into more attractive—but riskier—yields.

Without leverage, carry trades typically yield the interest rate differential minus broker costs, perhaps 2-4% annually in favorable environments. This resembles bond-like returns and wouldn't attract much attention on its own. Leverage changes the math dramatically. At 10:1 leverage, a 3% annual carry becomes 30% return on margin. At 20:1, it becomes 60%. These leveraged yields explain why carry trades attract significant capital when conditions appear stable. But leverage cuts both ways—the same multiplier applies to exchange rate losses. A 5% adverse currency move at 10:1 leverage wipes out 50% of your margin, potentially exceeding a full year's carry income in days or hours.

Keep In Mind: Calculating carry trade returns requires checking actual broker swap rates rather than theoretical policy rate differentials, understanding that leverage amplifies both carry income and currency risk, and maintaining realistic expectations that account for the gap between gross interest differentials and net returns after broker spreads and costs.

The Risks of Carry Trading

The carry trade looks deceptively simple on paper—borrow low, invest high, collect the difference. But the strategy carries substantial risks that have bankrupted traders, blown up funds, and created systemic stress in currency markets during crisis periods. The returns from carry trades accrue slowly, day by day, while the losses can arrive all at once in violent moves that erase months or years of accumulated income in hours. Understanding these risks isn't optional—it's the difference between implementing the carry trade as a sustainable strategy versus learning expensive lessons about why seemingly free money rarely stays free.

Risks of carry trading:

-

Currency depreciation can wipe out carry profits quickly, as even modest adverse moves exceed what weeks or months of interest income provide

-

A 5% currency move against your position can eliminate an entire year's worth of carry income depending on the differential

-

Sudden risk-off moves trigger simultaneous carry trade unwinding as traders globally rush to exit similar positions

-

Carry unwinds create self-reinforcing cascades where selling pressure causes further depreciation, triggering more selling

-

The funding currency typically appreciates during crises as traders buy it back to close positions, accelerating losses for those still holding

-

Leverage magnifies both carry income and exchange rate losses, turning modest currency moves into account-threatening events

-

At 10:1 leverage, a 10% adverse move wipes out 100% of margin—and currencies can move 10% surprisingly fast during stress

-

Interest rate changes can narrow or eliminate differentials, reducing or reversing the carry you expected to receive

-

Central banks can shift policy unexpectedly, with a single meeting potentially destroying the fundamental basis of your trade

-

Emerging market currencies offering the highest yields often carry the greatest depreciation and volatility risk

-

Liquidity evaporates in emerging market currencies during stress, widening spreads dramatically and making exits costly or impossible

-

Weekend gaps can trigger losses far beyond stop levels when markets open after unexpected news

-

Correlation among carry trades means diversifying across multiple pairs may not protect you during systemic risk-off events

-

The crowded nature of popular carry trades means everyone heads for the exit simultaneously when sentiment shifts

-

Black swan events like the 2008 crisis, the 2015 Swiss franc unpegging, or the 2020 pandemic crash can occur without warning

The Asymmetry of Carry Returns

The fundamental problem with carry trading is that returns and risks operate on completely different timescales.

Carry income accumulates gradually, credited to your account in small increments each night. Building meaningful returns takes weeks and months of holding positions and collecting interest. But losses can materialize in minutes during a crisis or unexpected announcement. This asymmetry means the carry trade often feels like picking up pennies in front of a steamroller—the income arrives slowly and steadily until the moment everything goes wrong at once. The strategy works beautifully during calm periods, generating consistent returns that make traders complacent. Then a risk-off event hits, and those same traders watch months of accumulated carry evaporate in a single trading session.

When Carry Trades Work Best

The carry trade isn't a strategy that works equally well in all market conditions—it thrives in specific environments and struggles or fails catastrophically in others. Recognizing when conditions favor carry trading helps you deploy the strategy at opportune times rather than fighting against headwinds that make the risk-reward unattractive. The ideal carry environment combines several factors that collectively reduce the probability of adverse currency moves while maintaining the interest differential that generates returns.

Conditions when carry trades perform best:

-

Low volatility environments where currency pairs trade in stable ranges without sudden large moves

-

VIX and currency volatility measures at subdued levels indicating calm market conditions

-

Stable interest rate differentials where central banks are maintaining consistent policy positions

-

Widening differentials where the gap between funding and target currency rates is expanding rather than contracting

-

Risk-on market sentiment when investors are comfortable taking on exposure and seeking yield

-

Strong global growth periods when economic stability supports higher-yielding currencies

-

Trending currency markets where the high-yield currency is appreciating, adding capital gains to carry income

-

Central bank policy predictability with clear forward guidance reducing surprise rate decisions

-

Low correlation among risk assets, allowing genuine diversification across carry positions

-

Ample global liquidity conditions that support risk-taking and yield-seeking behavior

-

Political stability in high-yield currency countries reducing event risk

-

Carry-friendly seasonality, with some research suggesting certain months historically favor the strategy

Reading the Environment

Successful carry traders develop the ability to assess whether current conditions support the strategy or suggest caution.

Monitoring volatility indicators like VIX, currency-specific volatility measures, and implied volatility from options markets provides insight into how stable the environment is likely to remain. Low readings suggest calm conditions that favor carry; rising readings warn of potential turbulence ahead. Central bank meeting calendars and economic data releases help you anticipate periods when policy shifts could narrow differentials or trigger volatility. Risk sentiment indicators including credit spreads, equity market behavior, and commodity currencies collectively signal whether the market is in risk-on mode that supports carry or risk-off mode that threatens it.

Pro Tip: Monitor the carry trade itself as a sentiment indicator—when USD/JPY and other carry pairs are trending steadily higher on stable volatility, the environment supports new carry positions; when these pairs start showing increased choppiness or sudden reversals, the market may be signaling deteriorating conditions.

Pro Tip: Pay attention to positioning data from sources like the CFTC Commitment of Traders report, as extremely crowded carry positions often precede violent unwinds when too many traders need to exit simultaneously.

The carry trade strategy generates its best returns during boring, predictable markets where nothing dramatic happens—the periods when financial news is quiet, central banks are on hold, and traders complain about lack of opportunity are precisely when carry trades compound steadily without the volatility events that erase accumulated income.

When Carry Trades Fail

The carry trade's biggest vulnerability is its tendency to fail spectacularly rather than gracefully. Unlike strategies that might underperform gradually, carry trades often collapse in violent moves that deliver losses far exceeding anything the accumulated interest income could offset. Understanding when carry trades fail—and recognizing the warning signs—can help you reduce exposure before the worst damage occurs or avoid entering positions when conditions are deteriorating.

Conditions when carry trades fail:

-

Risk-off market panics when fear replaces greed and investors flee to safe-haven currencies

-

Global equity market selloffs that trigger correlated unwinding across all risk-seeking strategies

-

Sudden flight to quality pushing capital into funding currencies like the yen and Swiss franc

-

Unexpected interest rate changes that narrow or reverse the differential your trade depends on

-

Central bank surprises where dovish pivots in high-yield countries or hawkish pivots in funding currencies destroy carry logic

-

Currency crises in high-yield countries causing rapid depreciation that dwarfs any interest income

-

Capital flight from emerging markets during contagion events affecting multiple countries simultaneously

-

Political instability, elections, or policy uncertainty in high-yield currency nations

-

Black swan events including financial crises, pandemics, wars, or other unpredictable shocks

-

Liquidity crises when market participants can't exit positions at reasonable prices

-

Flash crashes that trigger stops and margin calls before traders can react

-

Correlation spikes where all carry pairs move against you simultaneously, eliminating diversification benefits

-

Weekend gaps after news breaks while markets are closed, bypassing stop losses entirely

-

Margin calls forcing liquidation at the worst possible prices during cascading selloffs

Historical Carry Trade Collapses

Studying past carry trade failures reveals patterns that repeat across different crisis events.

The 2008 financial crisis remains the most dramatic example of carry trade unwinding. USD/JPY fell from above 110 to below 90 in months as the yen surged while traders scrambled to close positions. AUD/JPY collapsed from near 108 to below 60—a drop of over 40% that wiped out years of carry income in weeks. The 2020 pandemic crash triggered a similar dynamic, with the yen strengthening sharply as risk assets sold off globally. In both cases, the carry trade went from profitable to devastating with terrifying speed, and those using significant leverage faced total account destruction. The 2015 Swiss National Bank decision to unpeg the franc from the euro showed how a single announcement could cause instant 20% moves, blowing through stops and leaving traders with losses far exceeding their account balances.

Pro Tip: Watch for rising volatility in carry pairs even before broader risk-off events—increased choppiness and failed breakouts often precede major reversals as smart money begins reducing exposure.

Pro Tip: Reduce carry trade size or exit entirely when VIX spikes above 25-30 or when funding currencies like the yen start strengthening against high-yielders without clear explanation—these signals often precede full carry unwinds.

The carry trade strategy tends to fail exactly when you most need it to work—during market stress when your other positions may also be losing money, creating correlated drawdowns that can devastate portfolios concentrated in risk-seeking strategies.

Managing Carry Trade Positions

The difference between carry traders who survive market turbulence and those who blow up often comes down to position management rather than trade selection. Identifying attractive carry opportunities is only half the challenge—managing those positions through changing market conditions, protecting against sudden reversals, and knowing when to reduce exposure determines whether the strategy generates sustainable returns or occasional catastrophic losses. Effective carry trade management requires accepting that the strategy's steady income comes with tail risk that must be actively managed rather than ignored.

Position Sizing for Carry Trades

The leverage that makes carry trade returns attractive is the same leverage that destroys accounts during unwinds, making position sizing the most critical management decision.

DO size positions based on potential currency move risk, not just the carry income you want to generate.

DO calculate how much your account would lose from a 10-15% adverse currency move and ensure you can survive that scenario.

DO use lower leverage than the maximum available, keeping effective leverage at 3:1 to 5:1 rather than the 20:1 or higher that brokers permit.

DO leave substantial margin buffer so that normal volatility doesn't trigger margin calls that force liquidation at the worst times.

DO reduce position size when volatility indicators rise, cutting exposure as the probability of adverse moves increases.

DON'T size positions based on how much carry income you want—greed-driven sizing leads to blow-ups.

DON'T use maximum available leverage just because it's offered—the ability to take 50:1 leverage doesn't make it wise.

DON'T assume historical volatility predicts future volatility—sizing based on calm periods leaves you vulnerable when conditions change.

DON'T concentrate all capital in carry trades—maintain diversification across uncorrelated strategies.

Stop Placement Strategies

Stops protect carry trades from turning small losses into account-destroying events, but placement requires balancing protection against premature exits from normal volatility.

The challenge with carry trade stops is that currency pairs can be volatile enough to trigger tight stops regularly while still being profitable over time through accumulated carry. Place stops too tight and you'll get stopped out repeatedly, paying the spread each time and missing the carry income that would have accrued. Place stops too wide and a genuine reversal inflicts massive damage before you exit. Most carry traders use wider stops than directional traders would—perhaps 200-500 pips depending on the pair's volatility—accepting that each individual trade has substantial risk in exchange for allowing positions room to fluctuate while collecting carry. The stop represents your maximum acceptable loss on the position, sized so that hitting it doesn't devastate your account.

Scaling and Adjusting Exposure

Building and reducing carry positions gradually rather than all at once reduces timing risk and allows adaptation to changing conditions.

IF volatility indicators are low and conditions favor carry trades... THEN scale into positions gradually rather than establishing full size immediately, reducing the impact of poor entry timing.

IF your carry trade is profitable and conditions remain favorable... THEN consider adding to the position on pullbacks, but maintain disciplined total exposure limits.

IF volatility starts rising or funding currencies begin strengthening... THEN reduce position size proactively rather than waiting for stops to be hit during a full unwind.

IF a central bank meeting or major economic event approaches... THEN consider reducing exposure before the event when outcomes are uncertain, re-establishing positions afterward if conditions remain favorable.

IF your carry trade hits your stop loss... THEN accept the loss and don't immediately re-enter hoping for a bounce—wait for conditions to stabilize before reconsidering.

IF multiple warning signs cluster together—rising volatility, funding currency strength, risk-off sentiment... THEN exit or dramatically reduce carry exposure regardless of accumulated profits, as the environment is shifting against the strategy.

Monitoring Central Bank Policies

Carry trades depend on interest rate differentials, making central bank policy the fundamental driver that requires ongoing attention.

The carry trade strategy ultimately rests on the decisions of central bankers in both the funding and target currency countries. A dovish pivot from a high-yield central bank narrows the differential and often triggers currency weakness. A hawkish surprise from a funding currency central bank can eliminate the carry advantage while strengthening the currency you're short. Monitoring central bank communications, economic data that influences policy decisions, and market expectations for rate changes helps you anticipate shifts before they become official announcements.

Pay attention to forward guidance, inflation readings in both countries, and any signals that policy stances are evolving. When the fundamental basis for your carry trade—the interest rate differential—is threatened, reducing exposure before the official announcement typically produces better outcomes than reacting afterward when the market has already moved.

Making the Carry Trade Strategy Work for You

The carry trade strategy offers something most trading approaches don't—returns that accrue simply from holding positions, collecting interest day after day regardless of whether price moves in your favor. This steady income stream appeals to traders tired of strategies that only profit from correctly predicting direction. But the carry trade's apparent simplicity masks real complexity and substantial risk. The strategy works beautifully during calm periods, generating consistent returns that can make traders overconfident. Then market conditions shift, and those same traders learn that months of accumulated carry can vanish in days or hours during a risk-off unwind.

Balancing Yield with Risk

The carry trade belongs in your toolkit as one strategy among many, deployed when conditions favor it and reduced or abandoned when they don't.

Treating carry as a core strategy that runs constantly regardless of market environment invites eventual disaster. The traders who profit from carry over the long term are those who recognize it as situational—attractive when volatility is low, differentials are wide, and risk sentiment is stable, but dangerous when any of those conditions deteriorate. Building carry awareness into your trading means understanding how interest rate differentials affect the currency pairs you trade even when you're not explicitly running carry strategies. It means recognizing when crowded carry positioning creates vulnerability to sudden unwinds. And it means maintaining realistic expectations that carry income is compensation for bearing exchange rate risk, not free money generated from a market inefficiency. The carry trade strategy can enhance returns during favorable periods, but sustainable success requires the discipline to size positions conservatively, the vigilance to monitor changing conditions, and the humility to step aside when the environment turns hostile rather than hoping the steady income will continue indefinitely.